If you are researching the credit score to buy a home in Las Vegas 2026, this guide covers everything you need to know. A lot of buyers assume they need a perfect score to qualify, but that is not the case.

In reality, many buyers in Southern Nevada purchase homes with scores well below 700. What matters most is understanding how your score affects your loan options, your monthly payment, and your long-term costs. Whether you are looking in Summerlin, Henderson, or North Las Vegas, knowing where you stand puts you in control of the process.

Why Your Credit Score Matters

Your credit score is one of the main tools lenders use to evaluate risk. In a competitive market like Las Vegas, it does more than determine approval. It directly impacts how much you pay over time.

A stronger credit profile can help you in several ways:

- You may qualify for a lower interest rate, which reduces your monthly payment and total interest paid

- You can lower the cost of mortgage insurance if your down payment is under twenty percent

- You may gain access to higher loan limits and better financing options for more expensive properties

Even a small difference in your rate can translate into thousands of dollars over the life of your loan.

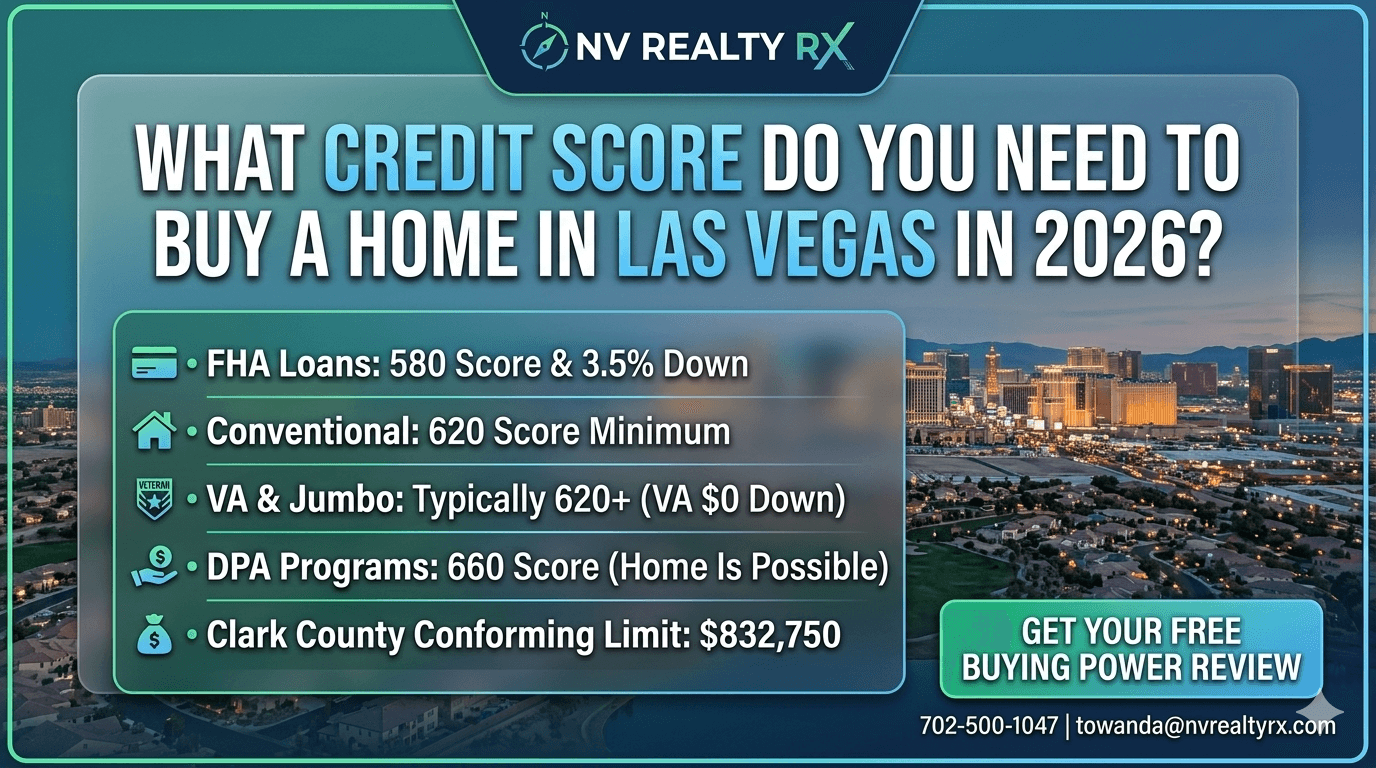

Credit Score Requirements by Loan Type

There is no single minimum score that applies to every buyer. Requirements depend on the type of loan you choose and the lender you work with.

Here is a realistic breakdown based on current 2026 lending standards:

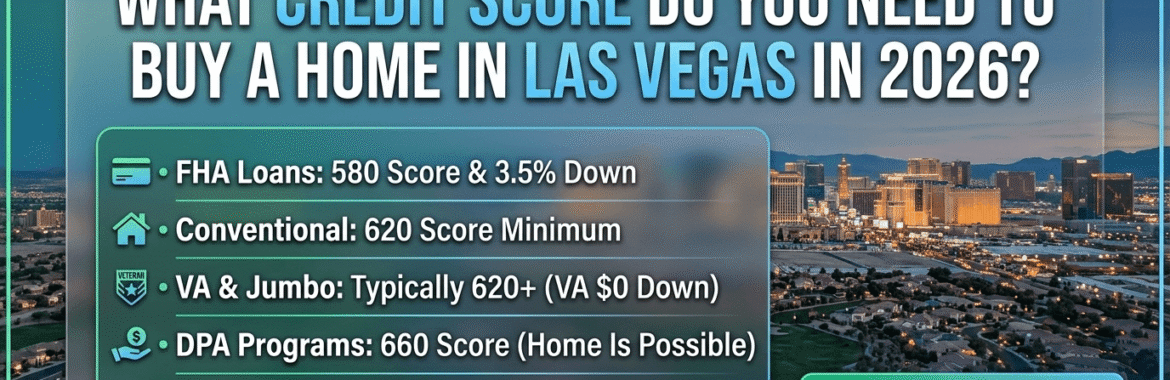

FHA loans

Most buyers can qualify with a score of 580 and a 3.5 percent down payment. Some lenders may require higher scores depending on the full application.

Conventional loans

Typically require at least a 620 score. Better rates are usually available once you reach the high 600s or above.

VA loans

There is no official minimum set by the Department of Veterans Affairs. However, most lenders look for a score around 620. Some may approve lower scores with strong compensating factors.

Jumbo loans

These are used for higher-priced homes above the conforming loan limit, which is around 832,750 in 2026 for most areas. Most lenders expect a score of 700 or higher.

USDA loans

Generally require a score around 640 and are limited to eligible rural areas. Some outskirts of Clark County may qualify, but eligibility should always be verified through the official USDA map.

How Your Credit Score Affects Your Payment

Your credit score has a direct impact on your monthly mortgage cost.

For example, on a 400,000 dollar home with a 30 year fixed loan, the difference between a higher and lower score can be significant.

A buyer with strong credit may secure a noticeably lower monthly payment, while a buyer with a lower score could pay more each month and significantly more in total interest over time.

In many cases, the gap can exceed 200 dollars per month and add up to tens of thousands of dollars over the life of the loan.

This is why improving your score even slightly before buying can make a meaningful difference.

What Lenders Look at Beyond Your Credit Score

Your credit score is important, but it is only one part of the full picture. Lenders evaluate your overall financial stability.

Debt to income ratio

Most lenders prefer your total monthly debt payments to stay within roughly 43 to 50 percent of your gross income, depending on the loan type.

Employment history

A consistent two year work history is typically required. This is especially relevant in Las Vegas, where many buyers work in hospitality, entertainment, or are self employed.

Property type

Condos and high rise buildings often have additional lending requirements. For conventional financing, the project usually needs to meet warrantable standards. It is important to confirm this early. Local costs

Property taxes, insurance, and HOA fees all affect your total monthly payment and buying power. Many master planned communities in Las Vegas include HOA fees, so these must be factored in from the beginning.

Down Payment Assistance Programs in Nevada

One of the biggest misconceptions is that you need a large amount of cash to buy a home. There are several programs in Nevada designed to help with upfront costs.

Home Is Possible

Offers assistance that is commonly structured as a second mortgage with no monthly payment. The amount is typically a percentage of the loan. Terms can vary, so it is important to review current program details with a lender.

Home At Last

Provides down payment assistance that can be used toward closing costs or upfront expenses. Credit score requirements generally start around 640.

Home First

Offers assistance that may be forgiven after a set period if occupancy requirements are met.

Program guidelines, funding, and rates can change, so always confirm the latest details before relying on them in your planning.

Common Credit Myths

Many buyers hold back because of outdated or incorrect assumptions.

You need a 20 percent down payment

Many loan programs allow much lower down payments, sometimes as low as 3 to 3.5 percent

Checking your credit will hurt your score

Initial prequalification checks are often soft inquiries and do not impact your score

You cannot buy with student loans

Lenders focus on your monthly payment, not the total balance

Final Thoughts

You do not need perfect credit to buy a home in Las Vegas. Many buyers qualify with average scores and stable income.

In many situations, buying sooner and building equity can be more beneficial than waiting years to improve your score while home prices continue to change.

The key is understanding your position and working with the right professionals to map out your options.

Ready to find out your true buying power?

Numbers and credit scores can be confusing, but you don’t have to navigate them alone. Get a Free 2026 Credit Analysis from a local Las Vegas mortgage expert.

See exactly which programs you qualify for today.

Get My Free Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}